Costanoa’s Amy Cheetham: Unlocking the Potential of B2B Financial Technology

Contents

ABSTRACT

🗒️

Amy Cheetham, partner and early-stage investor at Costanoa Ventures, argues that the pandemic — by driving demand for digital payment infrastructure — has opened the door to further opportunities in B2B fintech. Possible models include monetizing payment volume, lending, infrastructure services, and managing assets. Emerging markets, domestic SMBs, and insurance are all markets that need innovative products. Potential roadblocks include regulatory pushback and international risk.

KEY POINTS FROM AMY CHEETHAM'S POV

Why is B2B fintech such an important category moving forward?

The pandemic drove transactions online, pushing demand for digital-payment infrastructure, which in turn lays the groundwork for further digitization of financial services. “COVID had a significant impact on the fintech ecosystem, as more and more transactions had to move online. This created the need for improved online payment platforms, accelerating changes in what was already a quickly evolving landscape,” says Cheetham.

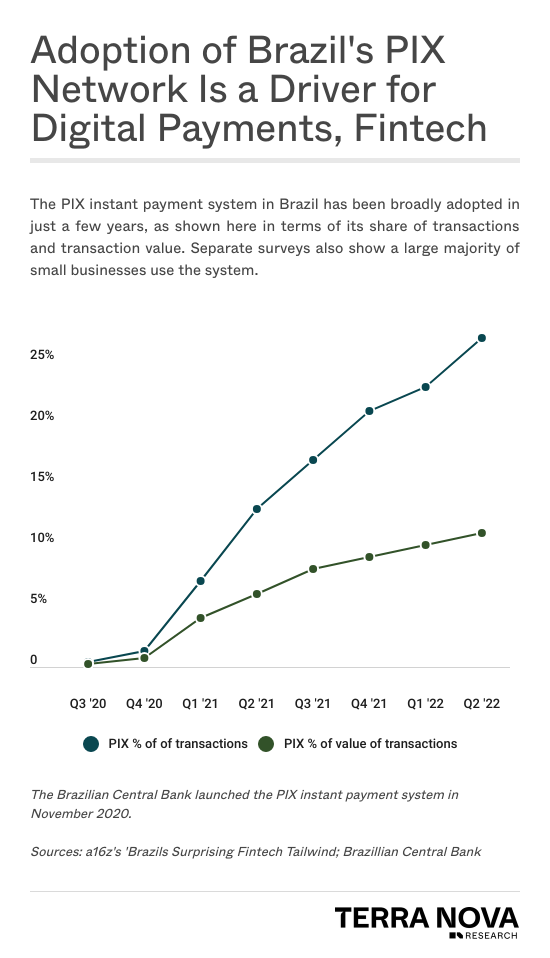

International markets could drive a large part of B2B fintech market growth, despite recent cool-downs in dealmaking. Latin America, with secular growth in tech adoption among businesses and consumers, is a hotspot. “Latin America has experienced significant growth in its fintech ecosystem,” Cheetham says. “It is uniquely positioned in the world for continued outsize growth, and could even outpace the US in some areas. In Brazil alone, digital payments have skyrocketed (see chart, below), and e-commerce penetration has increased by 74% year-over-year in 2022. While some investors have pulled back in the region due to the shifting macroeconomic environment, we remain bullish, particularly in Brazil given the economic, technological and regulatory factors there. That being said, of course markets like Brazil remain volatile environments, as we saw with recent political unrest in the region.”

While some investors have pulled back from Latin America due to the shifting macroeconomic environment, we remain bullish. In Brazil alone, digital payments have skyrocketed.

Amy Cheetham~quoteblock

What are examples of businesses that might be attached to this category?

The most appealing projects are innovating on payment and insurance tech infrastructure. “Our approach is generally to invest in the technology that sits behind consumer financial services offerings. We want to invest in the pipes and tools that allow consumer companies to create and sell innovative offerings,” says Cheetham. “As a result, we’ve focused on infrastructure in payments, insuretech, and fintech as the core tenets of our fintech practice.”

There are numerous ways to monetize B2B fintech.“We’ve seen so many models over the years across the fintech ecosystem, from monetizing payment volume to lending to infrastructure services and beyond. There’s a wide range of ways to monetize B2B fintech platforms.”

What are some of the potential roadblocks?

In the US, regulatory pushback may continue to challenge fintech players and their relationships with sponsor banks. Regulatory action has responded to misuses of bank charters and cases where fintech players failed to perform proper end-customer diligence. “While still common, the structure where fintechs work with sponsor banks has been the subject of debate,” says Cheetham. “I don’t believe this will be a significant challenge going forward, but the possibility for this sort of regulatory scrutiny could pose a risk to the sector.”

International risk is certainly there, given the bets in Latin America and other emerging market regions. “In the financial services sector, there is always a fear that regulatory changes will create headwinds, especially in more geopolitically volatile environments.”

Savvy investors will avoid companies that rely on volatile consumer preferences or the hype around fintech as an investment category. “Fintech has been a popular category, particularly in 2020 and 2021 when valuations reached their peak and money was pouring into consumer fintech and B2B fintech. That’s why we believe our approach of focusing on the B2B rails and infrastructure allows us to benefit from the hype without having to invest in products that are more driven by the whims of fickle consumers.”

VISUAL: INSTANT PAYMENT ADOPTION IN BRAZIL

IN THE INVESTOR’S OWN WORDS

Amy Cheetham

My focus is primarily on seed-stage B2B fintech companies, which encompass everything from fintech infrastructure to payments to application-layer tools such as CFO software suites.

We’ve seen a slow transition from banks as the only providers of financial services to more innovative offerings from fintechs becoming much more commonplace.

This evolution is still in the very early stages. We’re finally entering an era where banks’ monopoly on financial services is over.

Banks have become extremely vulnerable — they’ve lacked innovation for years and have taken their customers’ loyalty for granted instead of investing in new products and services. This has left them exposed and many are now playing catch-up to try to plug the hole that’s been opened by tech companies who are stealing their customers.

We’re slowly seeing the flow of money transition from being completely controlled by banks to being spread out across many types of technology companies.

All that said, we are still very much in the early innings of this transition. One data point that exemplifies the nascent nature of this market is that, while numerous neobanks have been launched in the last decade, only roughly 11% of the US population has a digital-only bank account. There is so much work to be done to provide far-reaching access to tech-forward financial products here and across the globe.

MORE Q&A

Q: How are you approaching your contrarian view on fintech investing into LatAm markets such as Brazil?

A: We’re continuing to be bullish on emerging markets while others are retreating. We believe the fundamentals in countries like Brazil remain strong despite weakening economic conditions in other regions. They’ve weathered high inflation and interest rates many times in the past and are set up well to prevail again. They have a highly collaborative regulatory structure that we’re confident will continue to promote and support innovation in the financial services industry.

Q: How do you decide involvement in a market where there may be several regulatory and consumer-dependent risks?

A: Building a company that will create long-lasting change in the financial services industry requires unique insights into a corner of the market that hasn't been disrupted effectively, combined with a differentiated distribution strategy. It's rare to see real innovation - often what we see are slightly updated versions of a previously created business model or strategy. When I see a truly distinct and novel idea, combined with a strong team with deep industry expertise capable of navigating the complexities of the regulatory environment, that's when I get excited.

I believe that SMBs remain a technologically underserved category.

Amy Cheetham~quoteblock

WHAT ELSE TO WATCH FOR

Look for more fintech products that specifically address underserved SMB markets. “I believe that SMBs remain a technologically underserved category,” says Cheetham. "Financial services targeting SMBs are still in need of continued innovation and investment. This has long been a core part of my thesis since I started investing back in 2015, and was part of the reason we led a Series A in Podium while I was at Summit Partners, which helps to provide payments to brick-and-mortar SMBs."

The 2022 EVC List honors the top 50 rising starts in venture capital. Terra Nova’s Thesis Brief series showcases each investor’s insights and category expertise.

Both enterprise and consumer are ready to adopt deep tech for consumer technologies as interest and spending in the space has become greater than ever before...

Over the last decade, the first wave of vertical software adoption transformed mainstream industries, including restaurants, home services, and salons....