Sapphire Ventures’ Demi Obayomi: Emerging Trends in Supply Chain and Logistics

Contents

ABSTRACT

🗒️

Covid-19 was the Black Swan event that brought supply chain resilience to the top of all stakeholders’ minds. In addition, market players are increasingly expected to deliver a modern customer experience, further making the supply chain & logistics category ripe for technological innovation. Demi Obayomi, vice president at Sapphire Ventures, examines the business models and tools that are emerging within supply chain & logistics as well as the industry headwinds that these new vendors must overcome.

KEY POINTS FROM DEMI OBAYOMI'S POV

Why is supply chain & logistics such an important category moving forward?

Covid-related supply-shocks have made supply chain & logistics one of the most pressing issues of today. Supply chain & logistics is the invisible lifeblood of the global economy. These processes are so mission-critical that the prevailing attitude is “if it ain’t broke, don’t fix it,” says Obayomi. Now that it’s clear the status quo will not suffice on a go-forward basis, industry players are more open than ever to evaluating and adopting new technologies that deliver on business outcomes. This gives startups a window of opportunity to play an outsized role in the modernization of global supply chain & logistics.

Shippers are demanding solutions, like supply chain visibility, that parallel the experiences consumers enjoy in their personal lives. “In the same way that we can keep tabs on our Amazon packages from order to delivery, customers are demanding solutions to track their multi-million dollar shipments from point to point,” says Obayomi. Supply chain visibility is the most prominent example of these new solutions. “When you consider the hierarchy of needs, the ability to pinpoint where valuable shipments are on the globe is a table stakes capability that shippers expect their logistics partners to provide,” he says.

The rise of digital-native competitors is forcing traditional logistics companies to adopt new technologies in order to stay competitive. The rise of tech-enabled logistics providers like Flexport, a ten year old freight forwarder born in Silicon Valley, has heightened the pressure on competitors to offer modern customer experiences. In addition to traditional services like securing ocean or air freight, Flexport has built its own software to streamline workflows such as exception management, document search & storage and business intelligence. “If you are a small freight forwarder,” says Obayomi, “you’re getting your lunch eaten by digital-native players like Flexport because they provide a modern experience that customers now expect.”

What are the business models that might be attached to this category?

In addition to SaaS, business models from financial services and insurance will play a key role in supply chain & logistics innovation. “Over a decade ago, outfitting a warehouse or factory with robots often meant a large upfront CapEx investment, which only the largest enterprises could afford,” Obayomi explains. In the last few years, many startup robotics companies have flipped this model on its head by offering customers the option to pay for robots on a subscription basis. Fast forward to today, the ability to monetize through financial services like payments or factoring has created an opportunity for vendors to take this idea to the extreme and offer their products at no upfront cost to the customer. “MVMNT is a recent example of this, offering its TMS software to brokers for free to gain access to as many brokers and as much freight volume as possible that can then be monetized through embedded financial services,” says Obayomi.

What are some of the potential roadblocks?

Conservative disposition of the supply chain & logistics industry draws out sales cycles, especially at the enterprise level. Many enterprises use a tangle of legacy systems from Oracle, IBM or SAP, as well as homegrown tools they built over time. The complexity of this set-up, along with the business risks associated with adopting a new solution creates enormous friction. “Sales cycles can be especially long because of the number of stakeholders involved,” says Obayomi. “The critical nature of manufacturing goods and moving them from point to point means that purchasing a new technology is a carefully considered process. No one wants to put their career on the line because they stuck their neck out for a system that ultimately proved ineffective.” Sales cycles can take six to nine months at large enterprises. The digitization of global supply chain & logistics may take longer than expected as a result.

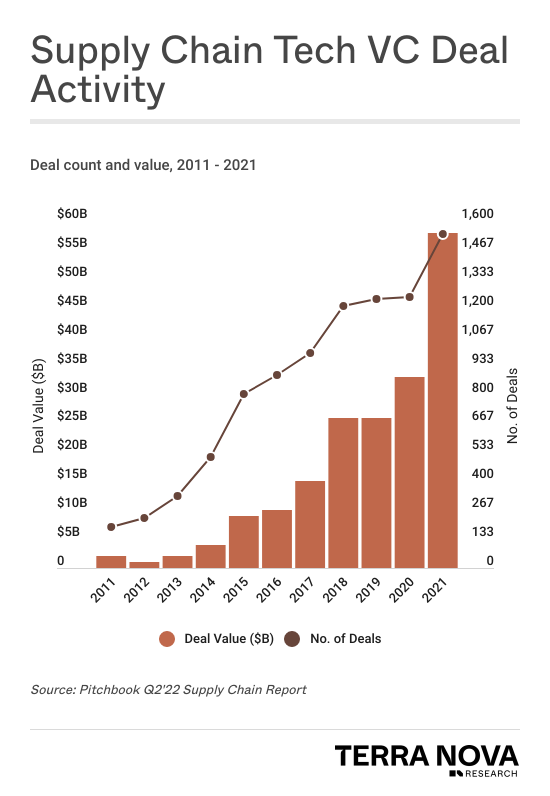

VISUAL: SURGE IN VC DEALS TO SUPPLY CHAIN TECH

VC interest and deal flow for tech-enabled supply chain solutions have been increasing since 2011, with a notable burst at the beginning of the pandemic. There has been a significant increase in deal value over the past five years, and again during the pandemic.

IN THE INVESTOR’S OWN WORDS

Demi Obayomi

Virtually every product and service around us has gone through a supply chain. When supply chain & logistics work well, they’re invisible. When they falter, it becomes a front-and-center issue for all.

Supply chain & logistics is inherently a laggard category, in terms of technology adoption, because of its crucial, mission-critical role in the global economy. The risk of adopting new products that could negatively impact business operations often dissuades companies from modernizing their processes. Covid-19 was a once in a generational catalyst that uprooted a longstanding attitude in the space of, ‘if it ain’t broke, don’t fix it.’

Covid-19 shattered this conservative disposition and turned it on its head. Not only were trivial items like printers and jigsaw puzzles out of stock, but major crises arose when supply chain challenges led to shortages in critical items like medical components and baby formula. Wave after wave of shortages forced companies to seriously consider how they could increase resiliency in their global supply chain & logistics footprint.

In many cases, the losses due to supply chain & logistics failures during Covid-19 finally outweighed the business risks associated with implementing new technology. Investors and enterprises alike are now spending more time examining new products and tools that can be used to digitize global supply chain & logistics processes.

MORE Q&A

Q: Do you see most of the new winners in this space being smaller, piece-meal solutions or being full-stack and holistically focused?

A: Many of the existing, incumbent systems are so ingrained into their customers' operations that it would be nearly impossible to completely replace them off the bat. Most of the new solutions we see are augmenting existing vendors either by providing a layer of data-driven insights & analytics or by offering add-on functionality that is important for the customer but non-core for incumbent vendors.

I don’t see anyone building a new full-stack supply chain management suite because the larger vendors are already so entrenched in this regard. The strategy for a new vendor is to provide functionality that these larger vendors don’t focus on. Over time, new vendors can continue to wedge their way into offering more and more of the existing functionality that the incumbent supply chain management suites provide.

Q: Which specific signals are you following to track shifts in the industry’s readiness to adopt new technology?

A: The biggest indicator here is the sales cycle. Once vendors start to see the six-to-nine month sales cycle shorten, that’s a very strong indicator for the maturity of a particular technology. At the end of the day, it doesn’t matter how much lip service the industry pays to technology, the proof will be in the rate of adoption.

Another signal is the sales process itself. This could mean, for example, whether customers still require extensive proof-of-concept projects and pilots before they commit to making a purchase. If a technology is solving such a painful need that customers are willing to dive in and at least start trying the solution, that would represent a shift in readiness to adopt. Eventually every technology should get to a point where customers won’t require months of POCs and pilots because the solution is proven and customers are already well-educated on it and are ready to adopt.

WHAT ELSE TO WATCH FOR

Automation tools can eliminate manual tasks and help contain staffing challenges. “Many supply chain & logistics teams are still heavily reliant on manual processes,” says Obayomi. “Staff are manning phones or stuck in email to complete the processes needed to get goods from point to point. There’s also the issue of personnel churn in these roles, especially in recent years, and the increased difficulty in filling these roles with people who possess the right skills,” he says. Various automation tools have appeared that help companies increase operational efficiency. Some, for example, extract information from documents and push the data into back office systems eliminating the need for manual data entry, while others automate basic customer support, enabling staff to focus on more complex cases or tasks. Automation should increase the efficiency of the workforce and simultaneously help enterprises remain resilient to staffing shortages.

Data interoperability will be crucial going forward as the industry adopts more technology solutions. Interoperability issues between existing systems and new tools are common in supply chain & logistics tech. “Incumbent systems from vendors like IBM, Oracle or SAP need to communicate with these newer products,” says Obayomi, “but they can be challenging to integrate with because they don’t always have easy-to-use APIs or other connectors.” Integration products have emerged to solve this problem, taking on the challenge of building integrations that enable them to serve as an intermediary layer between two systems that need to exchange data. “This allows supply chain & logistics tech vendors to create functional products without needing to take on the task of building integrations to each and every system a potential customer may be using,” Obayomi explains. He believes vendors who ease the integration process and minimize complexity are primed to succeed in the long-term.

For more insights into the state of supply chain & logistics tech, see Demi Obayomi’s recent market landscape here.

The 2022 EVC List honors the top 50 rising starts in venture capital. Terra Nova’s Thesis Brief series showcases each investor’s insights and category expertise.

AgeTech innovations span from Healthcare to Fintech. AI advancements are enabling streamlined health plan navigation, and personalized healthcare solutions that improve wellbeing while preserving independence....

Vertical AI SaaS presents a prime opportunity for startups, fueled by increasing customer dissatisfaction with legacy tools. Karthik Ramakrishnan, Partner at IVP, assesses opportunities for startups to disrupt traditional workflows that offer tremendous market potential....

Dave Mullen, Partner at SVB Capital, details why ‘Built Data’ – a coinage of Big Data in its next generation form – will be the critical mechanism that unlocks the power of AI for global enterprises....